Trump’s policies flood the swamp, crowd out economy’s ‘animal spirits’

(Originally published Oct. 16 in “What in the World“) The International Monetary Fund is worried U.S. government debt under Trump is out of control.

With Washington running the largest annual budget deficit of any rich nation, the IMF projects that U.S. government debt will rise to 125% of GDP this year, and surpass 143% by the end of the decade.

Trump’s tariffs have shifted $110 billion from U.S. consumers and businesses to the federal government since he imposed them, with another $30 billion a month moving from the private sector to the government. But that’s not enough to compensate for the $4.1 trillion the Congressional Budget Office estimates the tax cuts in Trump’s “One Big, Beautiful Bill” will add to the federal deficit.

The CBO has warned that the costs of servicing this debt could hurt long-term economic growth. The IMF appeared to concur, advising that reducing the overall debt would ease interest rates and stimulate funding to private-sector investment.

While the debt rises, the U.S. federal government has now been shut down for more than a fortnight amid a political standoff over healthcare subsidies. With paychecks from the nation’s largest employer stalled to most employees, economists at RSM now expect the shutdown to cut 1% off of U.S. GDP every month that it goes on. U.S. Treasury Secretary Scott Bessent said Wednesday the shutdown was costing the U.S. economy $15 billion a week.*

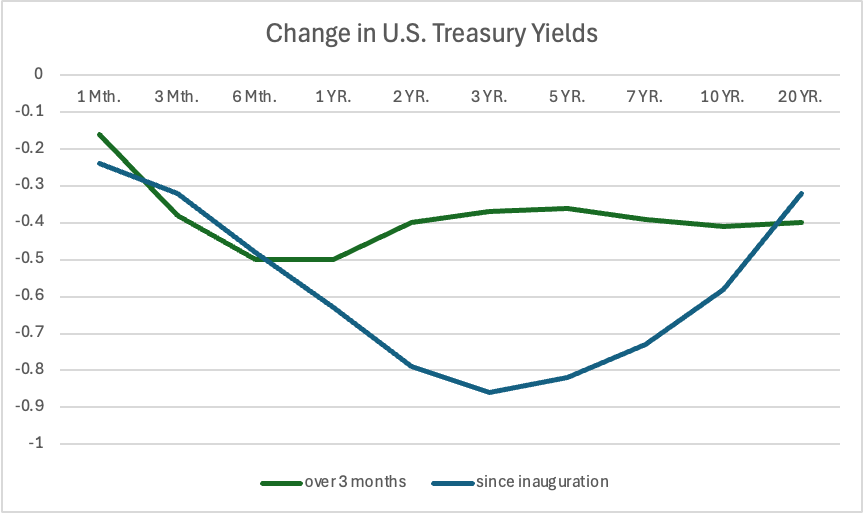

Bessent’s Treasury, meanwhile, has apparently been trying to lower government borrowing costs by shifting its bond sales from longer-term 10-year bonds to shorter-term 1-year T-bills. T-bills tend to have lower interest rates than longer-term bonds anyway since they represent an inherently lower risk of repayment. But what the Treasury is trying to do is reduce the supply of 10-year bonds on the market, thus pushing up their price and lowering their effective yield.

Is it working? Sort of. The yield on 10-year Treasuries has dropped roughly 40 basis points in the past three months to just over 4%, while the sudden surge in T-bill issuance has been offset by the Fed’s rate cut, pulling yields on 1-year T-bills down even further, by 50 basis points to just under 3.6%. The term premium has held fairly steady in the process, suggesting long-term expectations concerning growth and inflation haven’t much changed. The glut of T-bills also appears to be coaxing investors out of the 3- and 5- year segment they have favored since Trump took office.

But the shift to short-term debt raises Washington’s refinancing risks while sucking cash out of the economy. How? New Treasuries must be paid for in cash the day of settlement. Some $40 billion of such payments came due on Wednesday alone. Another $23 billion are due today.

Transfers of that magnitude put pressure on the amount of cash, or liquidity, that banks have available. When they run low, they turn to the Fed for short-term, usually overnight loans, ordinarily by selling the Fed a repurchase agreements (in which the Fed buys a security from a bank that promises to buy it back after a certain period of time at a higher price, i.e. a rate of interest—essentially borrowing money from the Fed, which thus injects cash into the financial system. But when banks ran into a liquidity crunch in 2021 during the pandemic, the Fed launched a new Standing Repo Facility (SRF) that banks can tap for emergency cash on top of that.

On Wednesday, when the $40 billion payment crunch hit, banks borrowed $6.5 billion from the Fed’s SRF — an indication that liquidity got pretty tight. And the interest rate on overnight repos climbed to 4.36%, its highest since the deadline for corporate tax payments last month created a similar liquidity squeeze.

What this suggests, in a nutshell, is that the government’s soaring funding costs are starting to overburden the U.S. financial system, potentially squeezing out its ability to maintain normal financing to the private sector.