Markets cheer Trump non-deal with net-importer UK; China, EU await

(Originally published May 9 in “What in the World“) Trump has so terrorized investors that even a small respite from his daily onslaught can spark a rally.

So it is with his latest trade deal with the United Kingdom—a country that runs a trade deficit with the United States. Hopes that the White House will now negotiate down Trump’s insane “reciprocal” tariffs with individual trade partners sent the benchmark S&P500 index up 0.58%.

The index remains almost 6% lower than when U.S. President Donald Trump took office. So perhaps markets, albeit tortured, remain clear-eyed: the U.K.-U.S. deal only marginally lowers the level of excrement into which Trump has plunged U.S. economic prospects. But, like his 90-day pause on reciprocal tariffs, it leaves both nations worse off than before. Americans will still have to pay a 10% tariff on all U.K. imports, which only account for 2.1% of U.S. imports anyway. And that’s if the deal, which is really only a framework for negotiating a detailed deal, succeeds.

And while Trump says his tariffs on China are likely to ease, it appears unlikely that U.S. Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer will come home from their jaunt to Geneva this weekend to meet China’s Vice Premier He Lifeng with little more than some Toblerone and a few thousand frequent-flier miles. As Bessent and Greer packed their power adapters for their Alpine weekender, China’s President Xi Jinping was in Moscow, pledging to stand with Russia against “unilateralism and hegemonic bullying behavior.”

Xi’s trip to Moscow doesn’t preclude a deal between Beijing and Trump to reduce tariffs on Chinese imports, which range as high as 245% on some goods. China accounts for 14% of U.S. imports, second only to Mexico’s 16%. Some of Xi’s previous pro-Russian pronouncements have turned out to have been lullabies before adopting more neutral positions between Moscow and Washington. Xi may still stand rhetorically by his “no-limits partnership” with Russian President Vladimir Putin and their shared opposition to U.S. hegemony. But Xi may also be on the verge of selling Putin out on aspects of Ukraine (where Beijing has still refused to openly support Russia) to win concessions from Trump on trade. While Washington’s perennial, bipartisan antagonism has pushed Beijing closer to Moscow, China and Russia have always been frenemies at best. So maybe Xi helps Trump push Putin to the table on Ukraine. Maybe takes some of Trump’s deportees as part of the bargain.

Trump must now also treat with the 27 members of the European Union, U.S. imports from which are roughly equal in size to those from China and Mexico. The EU has threatened to impose tariffs on €95 billion ($106 billion) of US exports if Trump fails to reach a deal with it. And any trade deal with the EU is almost certain to require greater clarity on Ukraine’s future and what role the U.S. will play in its security. Maybe Europe gets some tattooed American deportees, too. Who knows?

The best advice today thus seems to come from bond giant Pimco’s chief investment officer, Dan Ivascyn. Ivascyn was in Beverly Hills this week to attend insider-trading junk bond king Michael Milken’s cover version of the World Economic Forum’s annual gabfest of global elites in Davos, Switzerland. Pigeonholed by a reporter from the Financial Times, Ivascyn warned that, while Trump may negotiate tariffs down from their grossly miscalculated, “Liberation Day” extremes, it was unlikely that he’d roll them back completely and, thus, the odds of a recession remain.

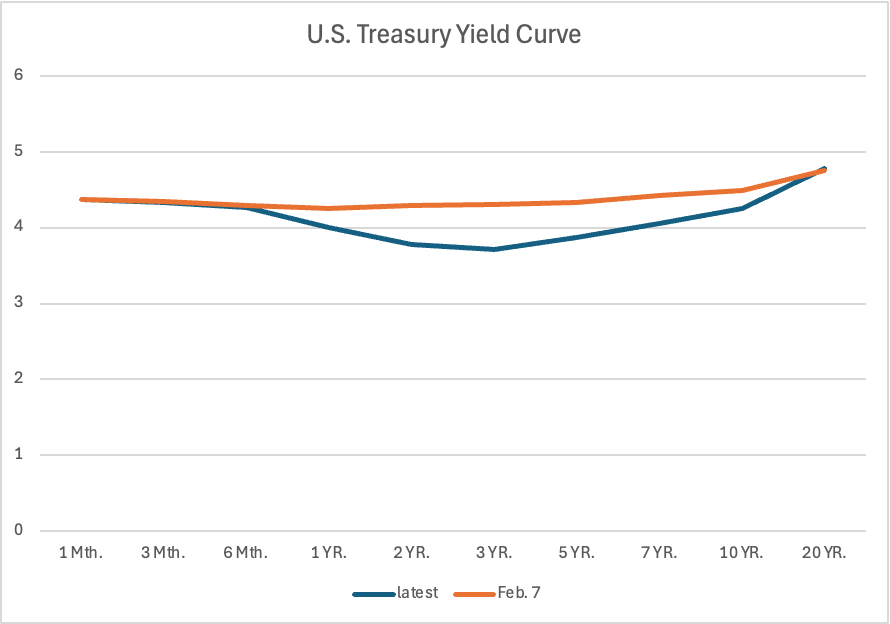

Ivascyn said that Pimco had been buying U.S. Treasuries, but shifting its portfolio (along with the rest of the market) into shorter maturities. Pimco has also been shifting into foreign government bonds, Ivascyn said.

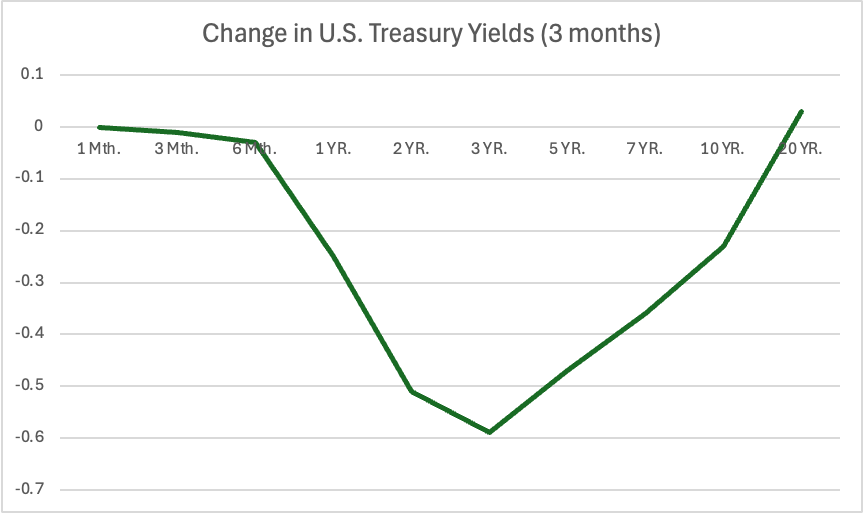

That trend has inverted the U.S. Treasury bond yield curve over the past three months.

With the sharpest decline in yields in 3-year maturities.

Trump, meanwhile, also appears to be rattled by his own policies so badly that he’s going Democrat. His latest policy proposal is to raise income taxes on the wealthiest Americans to 40%. Such a move would arguably help reduce the U.S. government deficit and narrow the widening U.S. wealth gap that arguably fuels the middle-class resentment that fuel’s Trump’s political support. But Trump’s proposed tax hike on people earning more than $2.5 million a year, would hit not only a key component of consumer spending, but also the small businesses that employ 43% of the U.S. workforce. Turns out that more than 90% of U.S. businesses are set up as “pass-through” businesses, in which the companies’ profits are paid out straight to their shareholders, who are then taxed on that income. Coming on top of his tariffs, his terror campaign against immigrants, and his evisceration of the federal bureaucracy, education, health, and scientific research, raising taxes right now on a key source of consumer spending and would only heap more hardship on the U.S. economy.